Your Crypto Loan Could Vanish Overnight: How DeFi Lending Really Works

Imagine borrowing against your house, but if prices drop 10% in an hour, your lender instantly sells your home to cover the debt. That's how crypto lending works today — and it's why thousands suddenly lose money during market swings. If you've ever used a savings account or taken a loan, understanding these risks matters because crypto lending skips banks but keeps all the danger.

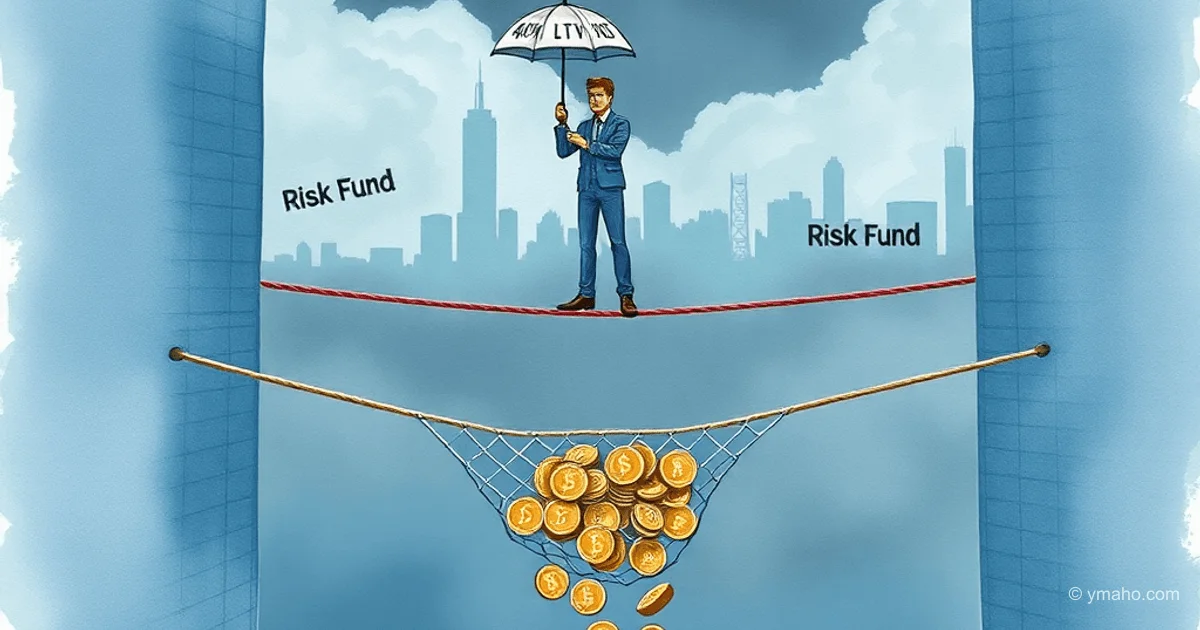

Why Your Safety Cushion Might Not Be Enough

In crypto lending, you borrow money by locking up digital assets as collateral (like using your house for a mortgage). The Loan-to-Value (LTV) ratio sets your borrowing limit — say 60% LTV means you can borrow up to 60% of your collateral's value. Think of LTV like a car's fuel gauge: the closer it gets to 'empty' (the liquidation threshold), the higher your risk of getting stranded. Higher LTV gives you more spending power but leaves less room for error when prices swing.

When crypto prices crash fast, your collateral's value drops. If it falls below a critical point (like a car skidding on ice), the system triggers automatic liquidation. Third-party 'liquidators' instantly repay part of your debt and grab your collateral at a discount — similar to how a repo man repossesses a car, but happening in seconds without human intervention. This protects lenders but can wipe out borrowers overnight.

The Emergency Fund That Sometimes Runs Dry

Protocols like Venus add a Risk Fund as backup — think of it as a neighborhood emergency fund built from small fees. It kicks in only during extreme crashes when liquidations don't cover all debts. But here's the catch: this fund has limited money. During the 2022 crypto crash, several protocols saw their safety nets drained as prices plummeted 30% in hours, proving even 'safe' systems can break under pressure.

What You Can Actually Do to Stay Safe

Unlike traditional loans with human negotiators, DeFi lending runs on cold, hard code. You're responsible for managing your own risk. Here's how regular people can navigate this:

- Keep LTV low: Borrow at 40% LTV instead of 80% to create a larger safety buffer

- Watch volatility: Avoid borrowing against 'meme coins' that can swing 50% in a day

- Set alerts: Use free tools to get SMS warnings when your LTV approaches danger zones

- Never max out: Treat maximum borrowing limits like speed limits — designed for ideal conditions, not real-world chaos

Key Takeaways

- LTV is your borrowing speed limit: higher = more risk of sudden liquidation

- Liquidation happens automatically during crashes, often at fire-sale prices

- Risk Funds help but aren't infinite — they're last-resort buffers, not guarantees

- Crypto lending removes banks but puts all risk management on you

What does this mean for regular people? DeFi lending can offer higher returns than banks, but it's like driving without seatbelts — fine until something goes wrong. Always borrow far below your limit, treat crypto volatility as a given (not an exception), and never risk money you couldn't afford to lose in an instant. These systems work beautifully in calm markets but turn brutal when prices swing, so plan like a cautious driver, not a racecar pilot.

— Editorial Team